Client

International: US cotton continued to fall sharply, and expectations of a large increase in planting area and good weather yields led to a large increase in production are gradually being digested. US cotton stocks are low, the number of unpriced contracts is still large, and the strong cotton printing, short-term US cotton ring to find support, pay attention to 68 cents / lb support.

Domestic spot: The transaction rate and price of the reserve have been lowered this week, mainly due to the decrease in the benchmark price and the decrease in the amount of Xinjiang cotton. Affected by the slump in foreign cotton, the base price of the reserve fell sharply by RMB 130/ton next week, and the national reserve cotton sales remained low. In terms of the total amount, domestic cotton supply is sufficient, while textile enterprises are entering the off-season, yarn prices are weak, textile profits are falling, and cotton demand is decreasing. Therefore, the current fundamental pressure on cotton is relatively high. However, the structural shortage of cotton in Xinjiang has not yet been resolved. In particular, the price of cotton produced in 2016 is still above 16,000 yuan/ton even if the price of cotton in the country is falling sharply. Therefore, the probability of price cuts is not large.

Domestic futures: US cotton continued to fall, Zheng cotton showed obvious resistance, down 15,000 yuan / ton, because Zheng cotton has a large discount of 800 yuan / ton compared to the deliverable cotton, the market price has increased significantly to support the disk, so the warehouse receipt is fast Flow out. Although the current cotton fundamentals are not optimistic, it does not rule out Zheng cotton's staged rebound to repair the discount. It is recommended to do more dips on the operation.

I. Cotton market one week market review

This week, ICE continued to fall, falling 4.77%. As of June 16, the US cotton index closed at 69.89 points/lb, down 3.5 cents/lb from last week. Zheng Mian also maintained its weakness, but it was stronger than the US cotton. The index closed at 15140, down 480 points from last week. The total position increased by 17,000 hands to 311,000 hands, and the turnover increased by 113,000 hands to 1.011 million hands.

Second, related information

(1) As of June 16, the country's cumulative processing of lint cotton was 5.037 million tons, a decrease of 22,000 tons compared with the same period of the previous year, which was 1.367 million tons less than the average of the past four years. Among them, Xinjiang processed 4.037 million tons of lint; cumulative sales of lint 4.63 million tons, a year-on-year decrease 369,000 tons, compared with the average of the past four years, 1.361 million tons, of which Xinjiang sold 3.728 million tons of lint.

(2) In the 16th week of the 2016/2017 reserve cotton round (June 19-23), the reserve price of the reserve cotton round was 15360 yuan/ton, down by 131 yuan/ton from the fifteenth week.

(3) The US Department of Agriculture announced the global cotton supply and demand forecast report for June, which raised the output of the United States by 440,000 tons to 4.18 million tons. The inventory consumption ratio was raised from 18% (the lowest in five years) to 32% in the current year; the output of China was increased by 270,000 tons. To 5.22 million tons, India raised 320,000 tons to 6.1 million tons, global production increased by 1.9 million tons to 24.98 million tons, and global consumption increased by 640,000 tons to 25.37 million tons. China's inventory consumption ratio continued to decrease to 103% from 128% this year, and the global rate was revised down from 78% to 75%.

Third, the fundamental analysis

1. Spot market

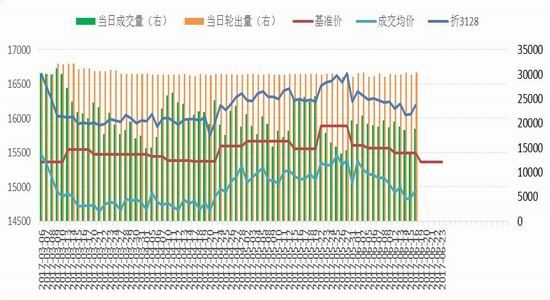

(1) National cotton storage

Figure 1: State stock auction results

Source: China Cotton Information Network, Luzheng Futures Research Institute

The reserve price of the reserve continued to decrease by RMB 68/ton, and the national reserve cotton volume decreased by RMB 150,000. The turnover was 91,000 tons. The weekly turnover rate was 61% lower than the previous month, and the average transaction price was RMB 14,904/ton. Yuan / ton. As of June 9th, the cumulative transaction rate of the national cotton storage was 69.6%, and the transaction volume was 1.51 million tons, of which Xinjiang cotton accounted for 65%. The benchmark price will continue to fall by RMB 131/ton next week, and the national reserve transaction price will continue to decline.

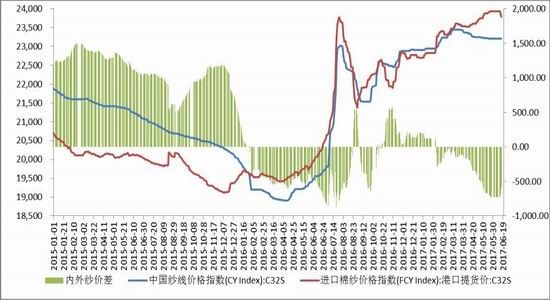

(2) Analysis of cotton prices inside and outside

In terms of spot, imported cotton prices fell sharply to below 15,000, while the inner cotton was weak and stable, and the spread between the two quickly expanded. As of June 16, China's cotton price index was 16004, down 72% from the previous month, and the port price of FCM was 14631 down by 631 points; Cotlook: A index was 14827. China's cotton price index (3128) did not increase the spread of the port price of 1360.

Figure 2: Inner and outer cotton price trends (yuan/ton)

Source: China Cotton Information Network, Luzheng Futures Research Institute

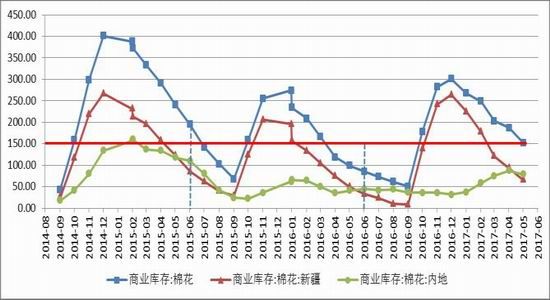

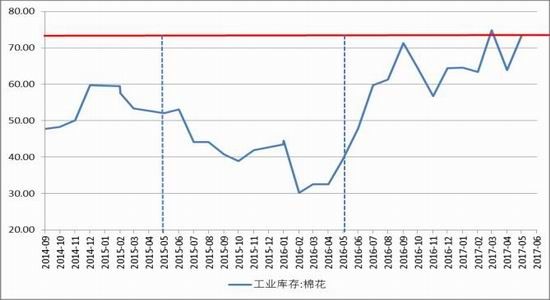

(3) Cotton stock

Commercial stocks are moderate and industrial stocks are high. By the end of May, the domestic commercial stock of cotton was 1.52 million tons, down by 350,000 tons, up by 520,000 tons; industrial inventory (spinning raw material inventory) was 730,000 tons, an increase of 90,000 tons from the previous month and an increase of 330,000 tons.

Figure 3: Domestic cotton commercial stock

Source: China Cotton Information Network, Luzheng Futures Research Institute

Figure 4: Domestic cotton industry inventory

Source: China Cotton Information Network, Luzheng Futures Research Institute

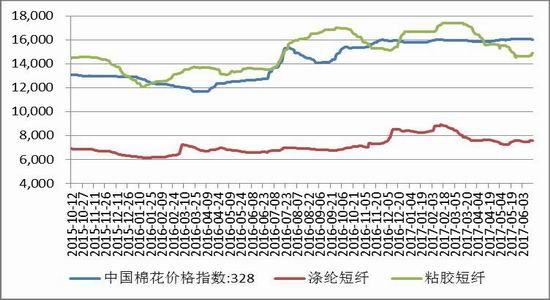

(4) Price trend of cotton and substitutes

Chemical Substitute Fiber: Both polyester and viscose have stopped falling, and their substitution for cotton has decreased. As of June 16, the mainstream prices of polyester and viscose changed by 756% and 14900 respectively, and the price difference of cotton non-chemical fiber was 8417 and 1104 respectively, which was converged with the cotton price difference.

Figure 3: Price trend of cotton substitutes (yuan/ton)

Source: WIND, Luzheng Futures Research Institute

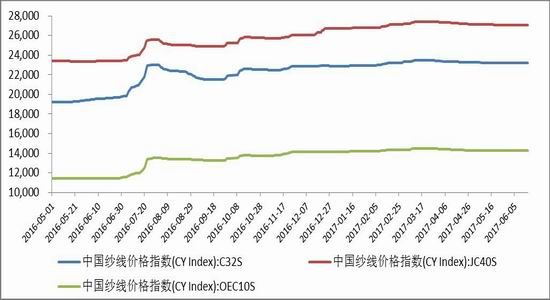

(5) Internal and external yarn price trends

Despite the fall in fabric prices, domestic yarn prices are stable. On June 16th, the price indices of C32S, JC40S and OEC10S were respectively 23210, 27050 and 14300, which were changed by 0, 0 and 0 points respectively.

Imported yarns began to fall rapidly, and the index is still higher than domestic yarns. The yarn price FCYC32S reported 23787, change -150. The yarn index is higher than the domestic yarn index of 577, which is still at a high level, and domestic yarn still has a competitive advantage.

Figure 4: Domestic yarn price trend (yuan/ton)

Source: China Cotton Information Network, Luzheng Futures Research Institute

Figure 5: Internal and external yarn price trends (yuan/ton)

Source: China Cotton Information Network, Luzheng Futures Research Institute

(6) Textile profit

The profit of new cotton spinning continues to fall, and combing is slightly better than carding. As of June 16th, the profit of JC40S ton yarn was lowered by 870 yuan/ton by 34%, while the C32S profit was 649 yuan/ton lower by 33.

Figure 6: Spinning high and low yarn profit trend (yuan/ton)

Source: Luzheng Futures Research Institute

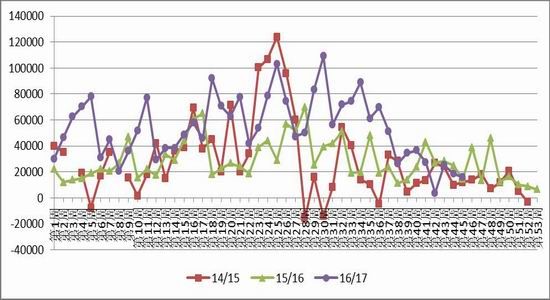

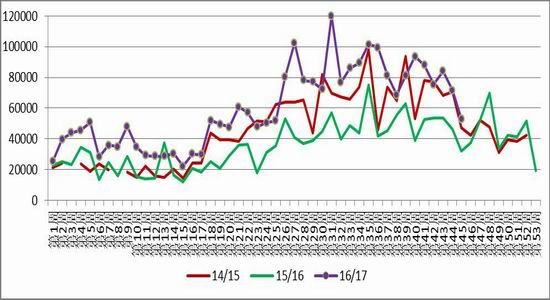

(7) US cotton exports

US cotton export contracting and shipments fell, but shipments remained high. The US Department of Agriculture report showed that on June 2-8, 2017, the net contracted volume of US cotton exports in 2016/17 was 1.57 tons, a 16% decrease from the previous week and a 16% decrease from the previous four-week average. The new signings were mainly from India (4763 tons), Vietnam (3515 tons), China (2721 tons) and Turkey (2517 tons).

In 2016/17, the shipment volume of upland cotton was 52,900 tons, which was 26% lower than the previous week and 34% lower than the previous four-week average. It is mainly shipped to Turkey (8958 tons), Vietnam (7938 tons), India (7529 tons), China (6463 tons) and Indonesia (4876 tons).

Figure 7: US cotton export week data (tons)

Source: USDA, Luzheng Futures Research Institute

Figure 8: US cotton weekly shipment data (tons)

Source: USDA, Luzheng Futures Research Institute

Cotton weekly

2. Futures market

(1) Internal and external cotton futures

Both inside and outside the cotton futures weakened, Zheng cotton was significantly stronger than US cotton, US cotton fell 4.77%, Zheng cotton fell 3.07%.

Figure 9: Inside and outside cotton prices

Source: WIND, Luzheng Futures Research Institute

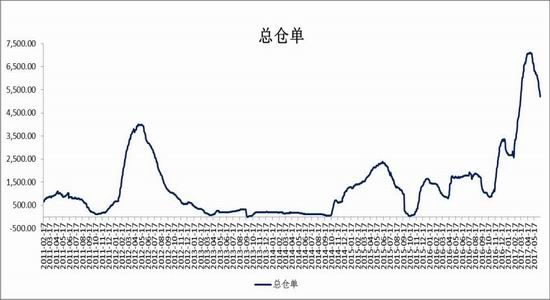

(2) Zheng cotton warehouse receipt analysis

Zheng cotton registered warehouse receipts decreased significantly and forecasts increased, and the total warehouse receipts continued to decrease but remained at a high level. The reduction of warehouse receipts due to the continuous decline of futures, the increase in market point orders, and the increase in forecasts due to the increase in the previous period of Zhengmian Chongao 16,200. As of June 16, Zheng Cotton registered 3,004 warehouse receipts, a decrease of 358 from last week, and an effective forecast of 1,404, an increase of 22 from last week. A total of 5,208 sheets, a decrease of 336 sheets from the previous week, and 211,000 tons of cotton lint, are still at a high level.

Figure 10: Zheng cotton warehouse single plus effective forecast (Zhang)

Source: Zhengshang Institute, Luzheng Futures Research Institute

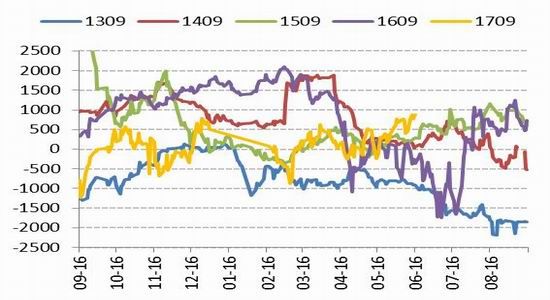

(3) Zheng cotton basis difference and spread change

This week's futures are weak, the basis continues to strengthen, futures are heavily discounted, and the 1-9 spread is lower. In September, the basis difference was between -700 and 700 for a long time. As of June 16, the CF1709 basis was stronger to 869, and the short-term exit was down.

Figure 11: Zheng cotton September basis

Source: Luzheng Futures Research Institute

Figure 12: Zheng cotton 1-9 spread

Source: Luzheng Futures Research Institute

(4) ICE period cotton funds face

Figure 13: ICE cotton non-commercial net multi-position

Source: CFTC, Luzheng Futures Research Institute

Speculative longs are still fleeing, and the US ICE cotton futures are falling. According to the latest report of the US Commodity Futures Trading Commission (CFTC), as of June 13, the ICE cotton non-commercial net long position was 75,544, which continued to decrease by 10044. The US cotton speculative funds were still mainly outflow.

3. Technical analysis

Zheng Mian: The volume of Masukura fell, the total position increased by 17,000 hands to 311,000 hands, the turnover increased by 113,000 hands to 1.011 million hands, the Masukura is not large, the amount of pressure on funds is still limited. On the weekly line, the price is strongly supported by the previous low of 15,000. There is support for the lower rail of Brin below. KDJ is already oversold, so the weekly line is facing a rebound. The daily line is in the lower edge of the shock zone, and it is facing a rebound in the short term.

Figure 14: Zheng Cotton Index Day K Line Chart

Source: Wenhua Finance, Luzheng Futures Research Institute

Figure 15: Zheng Cotton Index Week K Line Chart

Source: Wenhua Finance, Luzheng Futures Research Institute

ICE cotton: On the weekly line, the futures price has fallen continuously. It has already fallen below Brin's lower rail. KDJ is in an oversold state. Technically, the US cotton ring is facing a rebound. This week, we are concerned about the support of 68 cents/lb. Looking at the daily line, the futures price has entered the moving average, the space below is open, the indicator is weak, and it is in the search for support.

Figure 16: ICE Future Cotton Index Day K Line Chart

Source: Wenhua Finance, Luzheng Futures Research Institute

Figure 17: Weekly K-line chart of the ICE cotton index

Source: Wenhua Finance, Luzheng Futures Research Institute

Fourth, pre-judgment and next week's operational recommendations

International: US cotton continued to fall sharply, and expectations of a large increase in planting area and good weather yields led to a large increase in production are gradually being digested. US cotton stocks are low, the number of unpriced contracts is still large, and the strong cotton printing, short-term US cotton ring to find support, pay attention to 68 cents / lb support.

Domestic spot: The transaction rate and price of the reserve have been lowered this week, mainly due to the decrease in the benchmark price and the decrease in the amount of Xinjiang cotton. Affected by the slump in foreign cotton, the base price of the reserve fell sharply by RMB 130/ton next week, and the national reserve cotton sales remained low. In terms of the total amount, domestic cotton supply is sufficient, while textile enterprises are entering the off-season, yarn prices are weak, textile profits are falling, and cotton demand is decreasing. Therefore, the current fundamental pressure on cotton is relatively high. However, the structural shortage of cotton in Xinjiang has not yet been resolved. In particular, the price of cotton produced in 2016 is still above 16,000 yuan/ton even if the price of cotton in the country is falling sharply. Therefore, the probability of price cuts is not large.

Domestic futures: US cotton continued to fall, Zheng cotton showed obvious resistance, down 15,000 yuan / ton, because Zheng cotton has a large discount of 800 yuan / ton compared to the deliverable cotton, the market price has increased significantly to support the disk, so the warehouse receipt is fast Flow out. Although the current cotton fundamentals are not optimistic, it does not rule out Zheng cotton's staged rebound to repair the discount. It is recommended to do more dips on the operation.

Lu Zheng Futures Hou Guangming

Sina statement: Sina's posting of this article for the purpose of transmitting more information does not mean agreeing with its views or confirming its description. Article content is for reference only and does not constitute investment advice. Investors operate on this basis at their own risk.Men Canvas Belt,Men's Fashion Belt,Leather Men's Belt,Men Outdoor Canvas Belt

GDMK GROUP WEIHAI SHOES CO., LTD. , https://www.gdmkgroups.com